What is an equity loan and how does it work

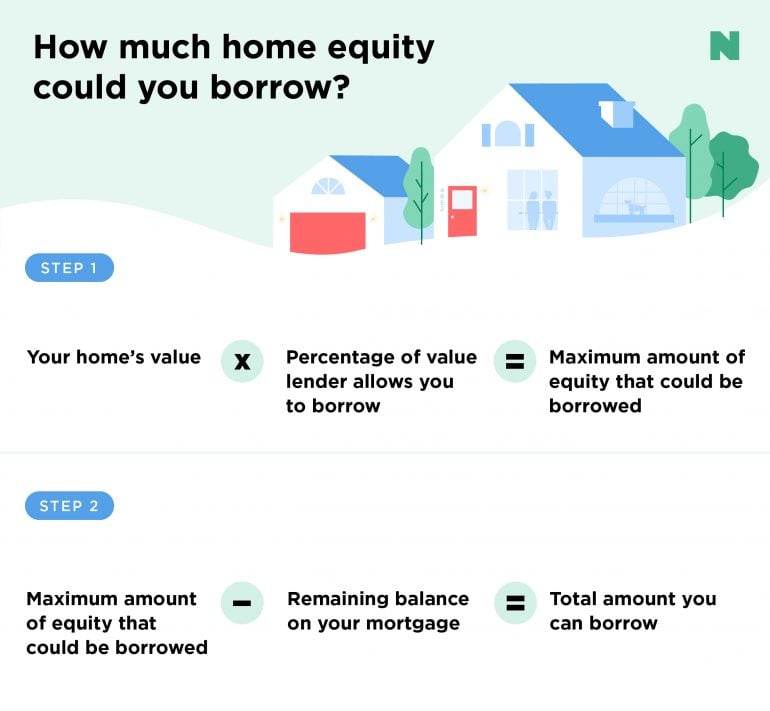

An equity loan is a type of loan that uses the borrower’s home equity as collateral. Home equity is the difference between the appraised value of the home and the outstanding balance on the mortgage. Equity loans can be used for a variety of purposes, including home improvements, debt consolidation, or other major expenses. The interest rate on an equity loan is usually lower than that of a traditional loan, making it a popular choice for borrowers who need to finance a large purchase. Equity loans are available in both fixed-rate and adjustable-rate options, giving borrowers flexibility in how they make their payments. Because equity loans are secured by the borrower’s home, they typically come with lower interest rates and more favorable terms than unsecured loans. However, if the borrower defaults on the loan, they risk losing their home to foreclosure. Because of this, people who want to take out an equity loan should think carefully about their ability to pay it back before signing a contract.

The benefits of consolidating your debt with an equity loan

If you’re struggling to make ends meet each month because of high-interest debt, you’re not alone. Millions of Americans are in the same boat, and it can be tough to find a way out. One option that may be worth considering is consolidating your debt with an equity loan. Discover the optimal location to finalize your loan using debt consolidation Here are some of the potential benefits:

First of all, consolidating your debt can help you save money on interest payments. When you consolidate your debts, you’re essentially taking out one big loan to cover all of your smaller loans. This can help to reduce the overall interest you’re paying since you’ll only be making one payment each month instead of several.

Secondly, consolidating your debt can help to simplify your financial life. Having just one loan to worry about can make it easier to stay on top of your finances and avoid missed payments or late fees.

Finally, consolidating your debt with an equity loan can free up some extra cash each month. Because you’ll be paying less in interest, you’ll have more money available to put toward other things like savings or investments.

If you’re considering consolidating your debt, an equity loan may be a good option to explore. Talk to a financial advisor to learn more about whether this strategy is right for you.

How to apply for an equity loan

Equity loans are a popular way to finance a wide variety of projects, from home renovations to starting a business. If you’re thinking of applying for an equity loan, there are a few things you need to know.

First, equity loans are typically only available to homeowners who have built up equity in their property. Equity is the portion of your home’s value that you own outright, and it can be used as collateral for a loan. To find out how much equity you have, just take the appraised value of your home and subtract the amount you still owe on your mortgage.

Next, you’ll need to choose a lender and apply for the loan. Be sure to shop around and compare rates before selecting a lender. Once you’ve been approved for the loan, the lender will send you the money in one lump sum. You can then use the money however you see fit.

Just remember that if you default on an equity loan, you could put your home at risk of foreclosure. So be sure to only borrow what you can afford to repay, and make all payments on time. With a little planning and preparation, an equity loan can be a great way to finance your next big project.

What to do if you’re denied an equity loan

A reverse mortgage is a type of home loan that allows homeowners to borrow against the equity in their home. Equity is the portion of the home’s value that is owned by the homeowner; it is calculated by subtracting the outstanding balance on the mortgage from the appraised value of the property. A reverse mortgage can be an excellent way to access the equity in your home, but it’s not always easy to qualify for one. If you’ve been denied an equity loan, there are a few things you can do to improve your chances of getting approved.

First, make sure you understand why you were denied. There could be some reasons, including poor credit, insufficient income, or too much debt. If you’re not sure why you were denied, ask the lender for more information. Once you know what’s holding you back, take steps to improve your financial situation. If your credit score is low, work on paying down your debts and establishing a history of timely payments. If you don’t have enough income to qualify for the loan, consider finding a co-signer or increasing your down payment. By taking these steps, you can improve your chances of getting approved for an equity loan.