Businesses use debit notes and credit notes as documents to adjust the particulars in the original invoices. The Goods and Services Tax (GST) law lays down a detailed provision for the issue of debit notes and credit notes. This article provides detailed information on debit notes and credit notes. It further elaborates on the GST Rules.

All about debit notes

All about credit notes

GST rules on debit notes and credit notes

How long should sellers retain credit notes and debit notes?

All about Debit Notes

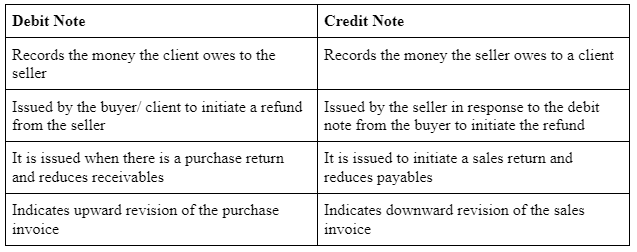

A debit note refers to a business document/voucher issued by a party to another one stating that such other party’s account is debited in the sender’s books.

A debit note is raised by a buyer on the seller if-

- The amount mentioned in the invoice is inaccurate

- They receive defective or damaged goods

- The value of the invoice is overstated

- The purchase of product/service is cancelled

- The goods received are not up to the buyer’s standards of quality

A debit note is raised by a seller on a buyer if-

- The amount payable to the seller rises

- The understatement of the invoice value

- The addition to the quantity of product or service

- The tax was undercharged on the invoice

For instance, a trader, M/s XYZ associates purchased goods from M/s PQR Ltd. After receiving the raw material, M/s XYZ associates found that the materials contained some defective goods valued at Rs.20,000. At present, M/s XYZ associates must reduce the liability standing in their books as payment due to creditor M/s PQR Ltd. Hence, M/s XYZ associates issue a debit note amounting to Rs. 20,000 to M/s PQR Ltd., stating that he has debited his account in his books.

Meaning Of Credit Note

A credit note refers to an invoicing document or voucher provided by one party to another party declaring that such other party’s account will be credited in the books of the sender.

It is not exactly a refund. However, it replaces the possibility of a refund whereby the purchaser can buy the products later without paying for them.

Continuing with the above example, the M/s PQR Ltd. finds that the material dispatched is defective. Hence, he issues a credit note to ABC to decrease the amount payable to the account of its creditor. It is the opposite of how a debit note works.

A credit note is issued for more than one reason, as follows-

- For any sales returns by the purchaser because of any product quality issues, rejection of services, or receipt of damaged goods.

- Incorrectly collected more charges from the purchaser or paid an amount higher than the invoiced value.

- Provide a discount after sales to the purchaser.

- The quantity of goods received by the purchaser is below the agreed one as mentioned in the tax invoice.

- The purchaser has cancelled any pending payment dues against invoices.

- Other similar reasons.

GST Rules on Debit Notes and Credit Notes

Section 34 of the CGST Act has covered rules about the need and procedure to use debit notes and credit notes.

There are reasons why debit notes and credit notes can be issued on separate occasions. They are as follows-

- Sales returns

- After-sales discount

- Service deficiency

- Invoice value corrections

- Please of supply changes

- At the time of finalising the provisional assessment

- Any other reason

There is no particular format defined under the GST law for debit notes or credit notes. However, you can get GST-compliant debit notes and credit notes generated with a button using professional invoicing software.

The debit note or credit note can be raised at any time. Accordingly, one can conclude that there is no time limit for issuing credit-debit notes. Further, credit notes and debit notes issued during a financial year must be reported in the GST returns in Form GSTR-1 filed periodically (either monthly or quarterly), delinked from their original invoice.

The law specifies a maximum period for reporting these notes in the GST returns. The details have to be reported by the below dates, whichever is earlier:

- The 30th September of the year following the end of the financial year in which such sale is made.

- The actual date of filing of the relevant annual GST return in Form GSTR-9

The following particulars should be noted-

(a) Name, address and Goods and Services Tax Identification Number (GSTIN) of the seller.

(c) Nature of the document.

(c) A consecutively designated serial number not more than sixteen characters, in a single or multiple series, consisting of alphabets, numerals or special characters, unique for a financial year.

(d) Issue date of the document.

(e) Name, address and Goods and Services Tax Identification Number (GSTIN) or registered Unique Identity Number of the buyer.

(f) Name and address of the buyer and the delivery address, together with the name of State and the state code, if it is a GST unregistered buyer.

(g) Serial number in original tax invoice, its issue date. Alternatively, the date of issue of a bill of supply and its serial number.

(h) Taxable supply value of goods or services, tax rate and the tax amount credited or debited to the buyer.

(i) Signature or digital signature of the seller or his authorised representative.

How Long Should Sellers Retain Credit Notes and Debit Notes?

The credit note and debit note documents must be retained for up to seventy-two months starting from the due date of filing the annual return for the financial year relating to such accounts and records.

Suppose such accounts and documents are retained manually. In that case, these should be stored at every relevant place of business noted down in the certificate of GST registration and must be accessible at every appropriate place of business where the company accounts and documents are digitally maintained.