Introduction

When beginning a replacement small business, an online store, or a contract side hustle, you will need to determine whether an LLC or a sole proprietorship is that the best legal structure for you and your requirements. From a legal, tax, and managerial standpoint, these two business models may make a giant difference in how you conduct your firm. According to Matthew Robertson from Business Fair Field, here’s all you need to grasp about sole proprietorships and LLC companies, still as the way to pick the simplest choice for your purposes.

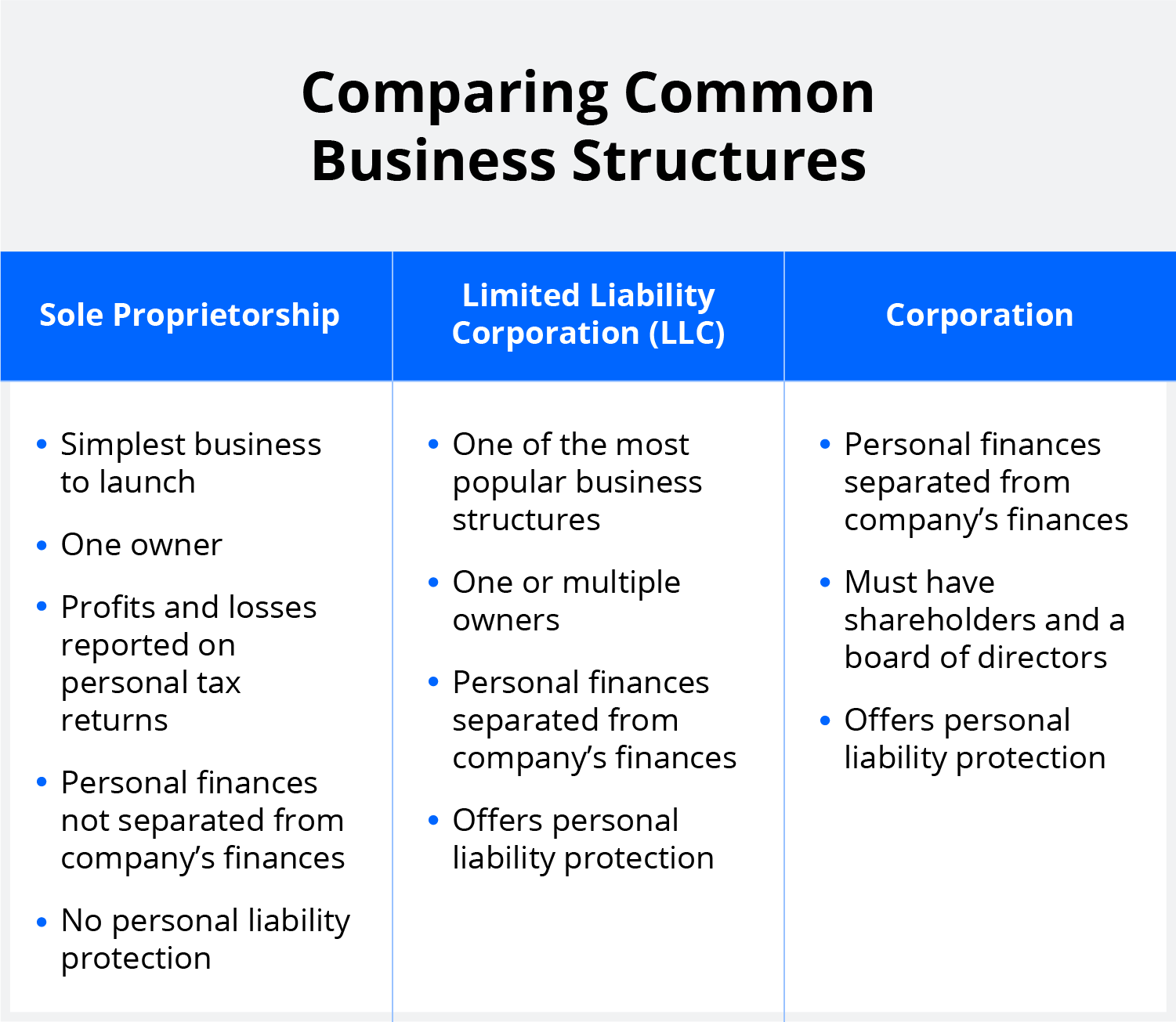

What is a Sole Proprietorship

A sole proprietorship may be a business that’s not incorporated and is owned by the one who runs it. for everybody who runs a business but hasn’t founded another official business structure like an LLC, a sole proprietorship is that the option. there’s no distinction between your personal and business assets and costs as a sole owner. you’re individually responsible for all debts and obligations incurred by your company.

There can only be one owner in a sole proprietorship. Your unincorporated business will be a general partnership if you hire a business partner.

What is an LLC

An LLC may be a form of company that’s formed by filing documents with the state. A indebtedness company (LLC) can have one or many homeowners (known as “members”).

An LLC has its own legal personality that’s distinct from you, the owner, after it’s founded. As a result, if your company is sued or fails to pay its obligations, a company creditor cannot lawfully pursue your personal assets. Furthermore, an LLC’s bankruptcy is regarded distinct from that of its owners. If you have got workers, an LLC may protect you from being held chargeable for their acts.

When comparing LLCs and sole proprietorships, entrepreneurs often seek out the expertise of the best LLC formation services to ensure a smooth and efficient process of establishing their business structure. These services provide comprehensive guidance and support for entrepreneurs looking to establish a solid foundation for their LLC.

Single-member LLCs are taxed the identical as sole proprietorships by default. An LLC, on the opposite hand, can better be taxed as an S Corporation or a C Corporation.

Formation

It’s possible that you’re running a sole proprietorship without even realizing it. By definition, anybody providing products and services without a partner is a lone owner. To legally run your single proprietorship, you may need to apply for business licenses or zoning permits, depending on where your firm is located. Any firm that operates under a trade name, including a sole proprietorship, must apply for a fake business name, commonly known as a DBA or “doing business as” certificate.

A limited liability company (LLC) may also need to apply for business permissions and a DBA. The articles of organization, on the other hand, are the most crucial formation document for an LLC. This document certifies the establishment of your LLC and must be submitted with the state in which you do business.

Management Structure

A limited liability company (LLC) can be owned by one or more members. An LLC is typically managed by its members, although they can alternatively designate a management to oversee day-to-day operations.

The membership of an LLC and the manner in which it will be operated are outlined in an operating agreement, which is a legal document.

In a single proprietorship, you are the boss and have complete control over your business. There are no associates or associates to deal with.

Taxes

In terms of taxation, a single-member LLC and a sole proprietorship are similar. Both are pass-through businesses, which means the company does not pay income taxes. The owner attaches a Schedule C to their personal tax return and reports business revenue, which is taxed at the owner’s personal income tax rate.

LLCs and sole proprietorships may have extra tax obligations in addition to income taxes. If you have employees, you must pay payroll taxes regardless of the business form you choose. If you sell taxable products or services, you must additionally collect state and local sales taxes. Finally, as a self-employed business owner, you must pay self-employment taxes to the Internal Revenue Service.

Personal Liability Protection

If your firm is sued, your personal assets are regarded “hands-off” when it comes to commercial debt collection or other claims. Creditors seldom have access to your house, car, or personal bank accounts.

There is no distinction between you and your business in a single proprietorship. All of the gains, as well as all of the debts and liabilities, are yours to keep. You might even be held liable for the liabilities that your workers produce.

So, Which Should you Choose?

Many entrepreneurs, particularly freelancers and consultants, begin as sole proprietors since it is the simplest option. There is no documentation necessary at the onset, and there is no significant financial investment, which is appealing to budding entrepreneurs, especially those who are testing a company idea. Sole proprietors also have it easy when it comes to taxes because they don’t have to submit a separate business tax return.

As soon as the business starts to develop, the rubber meets the road. Because a sole proprietorship provides no legal protection for your personal assets, you risk going bankrupt if your firm fails to meet expectations or encounters an unforeseen problem. In the case of a business bankruptcy or lawsuit, LLC owners aren’t individually accountable for the obligations of the company.

![[pii_email_bbc3ff95d349b30c2503]](https://publicistpaper.com/wp-content/uploads/2021/09/app-tips-microsoft-outlook-00-hero.jpg)